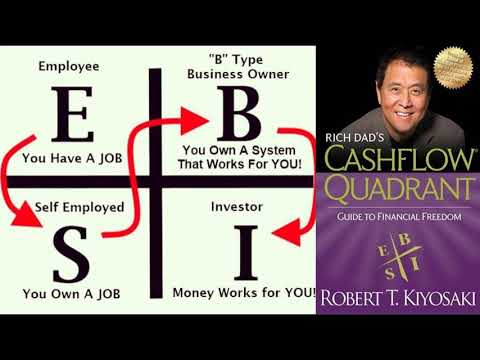

Rich dad’s cash flow quadrant written by a Robert T Kiyosaki with Sharon L Lecter CPA

Get your Copy at https://amzn.to/2WvkaUv